Net Worth vs. Income: What Matters More and Why

In personal finance, one of the most important questions is "net worth vs. income". The value of all your assets (things you own) minus any debts (liabilities) is your net worth. Net income, on the other hand, is the money you make over time from your job, business, or other sources. To make good financial decisions, you need to know the difference between these two metrics and how they work together.

Imagine gaining complete control over your finances, making every financial decision with confidence and precision. In 'Net Worth vs. Income: What Matters More and Why,' we delve into the crucial financial metrics that determine your wealth trajectory, ensuring you're equipped to build a more secure and prosperous future.

In the next five minutes, you'll gain insight into key financial concepts: net worth versus net income, their differences from annual income, and the steps to accurately determine your net worth.

What is Net Worth?

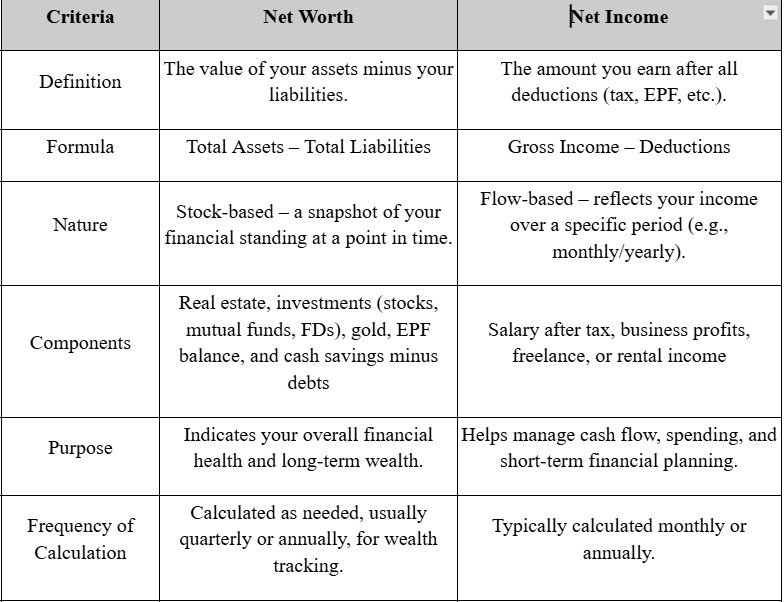

Net worth is also known as a measure of your wealth. Net worth is also the difference between your total assets and your total liabilities.

- Assets include cash savings, fixed deposits, mutual funds, stocks, retirement accounts, the value of your home or land, your car, your business, gold, and other similar investments.

- Liabilities include your home loan, car loan, personal loan, credit card debt, student loan, and other similar obligations.

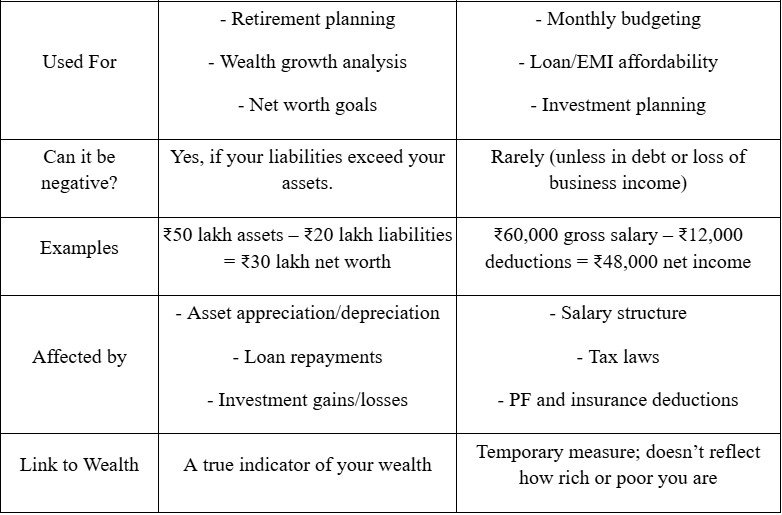

Imagine the relief of checking your finances and finding that your net worth is positive: it signals a sense of security, knowing you own more than you owe, giving you the freedom to plan for future investments or life goals without the weight of debt. On the other hand, a negative net worth can weigh heavily on your mind. Picture the stress of realizing your liabilities outpace your assets, like dealing with overwhelming credit card debt that demands careful planning and sacrifices to overcome. Once you have a list of these, subtract the total expenses from the total assets. That number tells the financial story: a positive figure means you have more than you owe, signaling financial stability, while a negative figure means you owe more than you own, adding to financial stress.

To monitor your net worth, you can use tools like the NSDL Consolidated Account Statement (CAS), as it consolidates all your holdings in one single monthly statement. Additionally, there are other tracking apps like Personal Capital, which offers in-depth investment tracking and budgeting capabilities, and Mint, known for its user-friendly design and comprehensive financial oversight. Personal Capital is better suited for those with investment portfolios due to its detailed analytics, while Mint excels in budgeting and everyday expense tracking. By comparing these options, you gain a sense of choice and control over your financial monitoring strategy.

What is Net Income?

The amount of money that remains in your bank account after all taxes are deducted from your average salary is known as net income, also referred to as "take-home pay". Your base pay plus any bonuses, allowances, or other payments you receive from your job make up your gross income. The actual amount of money you have available each month to invest, save, or spend is known as your net income.

To effectively manage this take-home pay, consider allocating a fixed percentage toward an automatic investment. This action not only makes the concept instantly usable but also helps you build a habit of consistent investing, which can significantly enhance your financial growth over time.

If your gross monthly salary is ₹60,000 and you have to pay income tax (₹4,000), EPF (₹7,200), and professional tax (₹200), your net income would be about ₹48,600. This is the amount you will get each month.

To put this into perspective, you might divide this amount using a basic budget formula: 50% for needs (₹24,300), 30% for wants or fun (₹14,580), and 20% for savings and investments (₹9,720). This approach helps in visualizing how your salary can be allocated effectively for daily life expenses, enjoyment, and future security.

Net Worth vs Net Income: Key Differences

Net worth and net income are two distinct yet important concepts in personal finance. They may sound the same, but they look at different parts of your financial health. Here are the key differences when it comes to net income vs net worth.

How to Determine Your Net Worth?

Knowing your net worth provides a clear picture of your financial health, allowing you to see exactly how much money you have available at present. Understanding your number can clarify how close you are to financial freedom, sparking the motivation to take action. Here is how to determine your net worth:

Step 1: List All Your Assets (What You Own)

Include everything of value that you own. This includes tangible assets such as real estate, vehicles, and investments. Don't overlook intangible assets like intellectual property or equity in side gigs, which can hold significant potential value. Some common examples:

- Real estate (house, land, commercial property)

- Bank balances (savings, fixed deposits)

- Investments (stocks, mutual funds, PPF, EPF, bonds)

- Retirement accounts (NPS, pension schemes)

- Gold and jewellery

- Vehicles (car, bike) — at current market value

- Any business ownership or valuable collectibles

The sum of all the above things will be the total assets.

Step 2: List All Your Liabilities (What You Owe)

Next, list all your outstanding debts or obligations:

- Home loan

- Car or two-wheeler loan

- Personal loan

- Education loan

- Outstanding credit card bills

- Any other EMIs or dues

Which of these debts could you eliminate in the next 12 months? Challenging yourself to rank your liabilities can spark proactive planning and help create a solid payoff plan.

The sum of all the above things is the total liabilities.

Step 3: Apply the Formula

Formula: Net Worth = Total Assets – Total Liabilities

For example:

- Total Assets = ₹70,00,000

- Total Liabilities = ₹25,00,000

- Net Worth = ₹70,00,000 – ₹25,00,000 = ₹45,00,000

How To Determine Your Net Income?

Understanding how to determine your net income can help you know what is the exact amount that you take home after all the deductions. It can be helpful in budgeting, saving and financial planning. Here is how you can determine your net income:

Step 1: Calculate Your Gross Income (Before Any Deduction)

This would include all your income sources before any kind of deduction. The sources can includes, Monthly Salary, Freelancing or side gig income, Bonuses, Incentives, Rental income, Interest or dividend income, and Other income sources. What skills could you monetize this quarter to boost gross income? Identifying and expanding potential earnings can significantly contribute to your net-income calculation.

- Monthly Salary

- Freelancing or side gig income.

- Bonuses

- Incentives

- Rental income

- Interest or dividend income

- Other income sources

The sum of these would be the gross income.

Step 2: Subtract Deductions and Taxes

The next step is to subtract mandatory and voluntary deductions from the total gross income. Below are some of the deductions:

- Income Tax

- Employee Provident Fund

- Professional Tax

- Insurance premiums

- Pension contributions

- Loan EMIs

- Salary deductions

- Other deductions

The total of all these deductions is the total deductions.

Step 3: Apply The Formula

The formula to calculate Net income is: Gross Income - Total Deductions

Let's take an example.

- Gross income = ₹10,00,000

- Total deductions = ₹2,00,000

- Net income = ₹10,00,000 - ₹2,00,000 = ₹8,00,000.

What Matters More? Net Worth or Net Income

The importance depends on the stage of life you are in. In the early stages of your career, you can focus on growing your assets by investing your surplus income. In simple terms, the more your net income is, the more you will be able to invest, and thus the more your net worth will be.

Consider the following stage-based checklist to understand where you stand:

20s: Focus on building income by investing in skills and career development. Start saving and explore investment opportunities that grow with time.

40s: Fortify your assets by focusing on asset growth and reducing debt. Diversifying investments ensures long-term security.

60s: Prioritize income generation from your accumulated assets. Plan for retirement and ensure that your investments support your desired lifestyle.

Although you will have to change your strategy and focus on generating tax-efficient income from the accumulated assets in the later stages of your life, as you age, you must focus on your net worth, as your assets will probably be the main source of income.

So, both aspects matter at different stages in your life.

Conclusion

Net worth builds the house, but net income pays the bills. Your net worth shows how stable and independent you will be financially in the long run, while a steady income can help you pay for daily expenses. Even if you make a lot of money, you could have a low or even negative net worth if you don't know how to handle your money well. That's why only thinking about money is like running on a treadmill: you might be moving, but you might not be getting anywhere. Stop worrying about how to make more money and start thinking about how to keep and grow what you already have. When it comes to financial freedom, what you own is just as important as what you make. In short, considering the difference between net worth and net income, net worth is equally important as net income. To take a proactive step towards financial stability, calculate your net worth today using the steps outlined above, or find ways to increase your net income, enabling you to invest more toward building wealth. Choose one path or both, and turn your financial insight into momentum for a more secure future.

FAQs About Net Worth vs Net Income

Can someone have a high income and a low net worth?

Yes. If expenses are high or money is poorly managed, a person earning ₹20 lakh annually can still have minimal or even negative net worth due to debts and zero savings.

How often should I check my net worth?

It is best to review your net worth every 6 to 12 months. This helps track progress, assess financial decisions, and stay aligned with long-term goals.

Should I focus more on growing income or building net worth?

Both matter, but building net worth offers financial security. Use your income to create assets, pay off liabilities, and invest wisely to grow your net worth over time.

Can my net worth be negative?

Yes, if your liabilities exceed your assets. For example, if you have loans of ₹40 lakh and assets worth ₹30 lakh, your net worth is –₹10 lakh.

Get Expert Financial Advice

Book an introductory call with our Certified Financial Planner to explore how we can help you achieve your financial goals.

Book Your Appointment