RSUs for Indian Employees: Taxation, Diversification & Strategic Wealth Planning

Introduction

In recent years, Restricted Stock Units (RSUs) have become a common component of compensation for Indian employees working at multinational companies, especially in technology and finance. RSUs are more than a reward — they signify ownership in the company, aligning employee performance with shareholder value.

However, many professionals remain unsure about how RSUs function and how they are taxed in India. Unlike regular salary or bonuses, RSUs are taxed in two stages — first as part of your income when they vest, and later as capital gains when you sell them. Understanding this process can help you make more informed, tax-efficient financial decisions.

What Are RSUs and How Do They Work?

Restricted Stock Units are company shares granted to employees as part of their overall compensation. The key difference between RSUs and stock options (ESOPs) is that RSUs don’t require any purchase — they are awarded no cost once certain conditions are met.

When you are granted RSUs, you don’t receive the shares immediately. They vest over time according to a vesting schedule.

For example:

- Grant: 400 RSUs are granted on 1st January 2024.

- Vesting Schedule: 25% vests at the end of the first year (1-year cliff), and the remaining 75% vest monthly over the next three years.

- Vesting Condition: You must remain employed through each vesting date to receive those shares.

Once vested, the shares are either credited to your brokerage account or sold on your behalf by the employer (depending on company policy).

Taxation of RSUs in India

RSUs are subject to taxation at two stages - at vesting and at sale. Let’s look at each in detail.

- Tax at the Time of Vesting

At the vesting date, you officially own the shares. The Fair Market Value (FMV) of the shares on that date is treated as a perquisite income under the head “Income from Salary.”

- The FMV (converted into INR) is added to your total taxable salary.

- Your employer usually deducts TDS on this value, similar to regular salary tax.

- The FMV on vesting becomes your cost of acquisition for future capital gains calculations.

Example:

If 100 shares vest on 1st January 2025 when the fair market price is $100 per share, and the exchange rate is ₹83 Per $, your taxable perquisite is ₹8,30,000 (100 × $100 × ₹83). This amount is taxed as salary at your applicable slab rate.

2. Tax at the Time of Sale

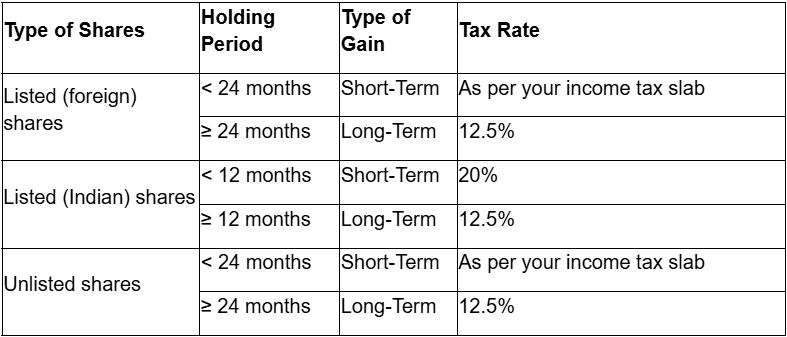

When you eventually sell the vested shares, you pay capital gains tax on the difference between the sale price and FMV (at vesting).

The rate and classification of capital gains depend on how long you hold the shares after vesting:

Example:

Continuing the previous example, if you sell your shares in 2027 at $130 each, you earn a gain of $30 per share. That $30 (₹2,490 per share approx.) is taxed as capital gains — short-term or long-term depending on your holding period ₹1.25 Lacs of LTCG exemption not applicable for foreign listed shares.

If any tax like U.S. withholding on vesting or dividends is paid abroad, you can claim foreign tax credit in India under DTAA provisions (e.g., India–US treaty). As an Indian resident, you must disclose: Schedule FA in your ITR for foreign assets (including RSUs/foreign stocks) even if not sold. Capital gains go in Schedule CG of the tax return.

To summarize:

- At vesting: Taxed in India as salary.

- At sale: Capital gains taxed in India.

- If US capital gains tax is withheld, FTC can be claimed in India under DTAA.

Proper documentation (Form 67, foreign tax statements, broker statements) is essential to claim foreign tax credit.

Common Pitfalls and Planning Tips

While RSUs can significantly boost your wealth, they come with some key considerations:

- Tax at Vesting – Even Without Sale

You are taxed at vesting even if you don’t sell your shares immediately. If the share price falls later, you may face a situation where you paid tax on a higher value than you eventually realize.

2. Liquidity Challenge

Since RSUs are not tradable before vesting, they cannot be liquidated early to cover taxes. It’s important to plan liquidity in advance to meet your tax obligations. if your company does not automatically sell shares to cover tax, you may need to fund the tax liability from personal cash flow.

3. Concentration Risk

RSUs increase exposure to your employer’s stock. Overreliance on a single company’s performance can increase your overall portfolio risk.

4. Currency Risk Exposure

Because these are foreign shares, both equity performance and exchange-rate movements affect your returns.

Let’s See Currency Risk in Action

Assumption (Initial Investment)

- Investment = $10,000

- USD/INR (2 years ago) = ₹83 per USD

Initial investment in INR:

$10,000 × ₹83 = ₹8,30,000

Case 1: USD strengthens

After 2 years:

- Share price remains $100 (no stock gain)

- USD appreciates to ₹100

Sale value = $10,000 × 100 = ₹10,00,000

Capital gain in INR:

₹10,00,000 – ₹8,30,000 = ₹1,70,000 gain

Even though the stock price didn’t move in USD, the investor made a gain purely due to currency appreciation.

Case 2: USD weakens

After 2 years:

- Share price remains $100

- USD falls to ₹70

Sale value = $10,000 × 70 = ₹7,00,000

Capital loss in INR:

₹7,00,000 – ₹8,30,000 = ₹1,30,000 loss

No stock loss in USD terms, but the INR investor suffers a capital loss due to currency depreciation.

5. Reporting Requirements

Foreign shares and accounts must be disclosed in your Indian tax return.

ADVISOR’S CORNER : Practical Strategies to manage & diversify RSUs

- Create a sell discipline (e.g., sell 30–50% on vesting to de-risk)

• Integrate RSUs into overall asset allocation - What % of your wealth is in RSUs? >30% is considered heavily allocated and active diversification is recommended.

• Use RSUs to diversify globally - broader indices, tech or non-tech sectors, emerging trends, etc.

• Align vesting schedule with long-term goals (education, retirement corpus, etc.)

Why is diversification important?

Redeeming RSUs periodically and diversifying across asset classes, sectors, and geographies helps reduce concentration risk, improves risk-adjusted returns, and smooths portfolio performance across market cycles. If the RSU share value declines significantly and a large portion of net worth is tied to it, overall wealth can fall materially, potentially delaying key financial goals such as retirement, purchasing a home, or funding a child’s education. It may also disrupt liquidity planning and lead to emotional decision-making during periods of sharp market corrections.

Integrating RSUs into Your Investment Plan

At FinAtoZ, we often advise clients to view RSUs not as standalone rewards but as part of a broader financial strategy.

When your RSUs vest:

- Set aside a portion of proceeds to meet your tax obligations.

- Reinvest part of your post-tax amount in diversified instruments to balance risk and pursue long-term goals.

- Maintain a clear record of FMV on each vesting date, since it determines your cost basis for future capital gains computation.

Ways to Diversify Beyond RSUs

Now the question arises - what investment options are available for such diversification? There are several structured avenues:

- Simple Domestic Mutual Funds: Provide diversified exposure across market caps and asset classes.

- AIFs via GIFT City: Offer access to global markets within a structured framework, helping add geographical and currency diversification.

- Global ETFs or International Feeder Funds: Enable exposure to international indices and sectors, spreading risk across countries and currencies.

- SIFs (Conservative / Hybrid / Aggressive): Structured strategies that range from low-volatility capital preservation to higher-growth tactical approaches, depending on risk appetite.

However, at the end of the day, the right mix depends primarily on your financial goals, time horizon, age, risk tolerance, existing asset allocation, and liquidity requirements. Diversification should not be product-driven, but goal-driven and aligned with your overall financial plan.

Conclusion

RSUs are a powerful wealth-building tool, linking your compensation to your company’s long-term success. But they also introduce complexities around taxation, timing, and diversification.

Understanding the two-stage taxation as salary at vesting and as capital gains at sale helps you plan better and avoid surprises during the filing season. Equally, diversifying your RSU proceeds into different investment products and across asset classes can convert concentrated stock exposure into a more balanced portfolio.

In short, while RSUs can be a rewarding component of your compensation, thoughtful financial and tax planning ensures that they contribute effectively to your long-term wealth goals.

Get Expert Financial Advice

Book an introductory call with our Certified Financial Planner to explore how we can help you achieve your financial goals.

Book Your Appointment