Financial Advisor - How much fees is justified?

Are you wondering how much fees is justified for your financial advisor? What is the value that your financial advisor adds to your overall financial journey? Does your financial advisor charge you too much for the financial plan and the investment advice that she gives you? How do you segregate between the value of investment advice and the service that your financial advisor provides you?

In our experience we have seen that most of the investors have similar questions at the top of their head while hiring a financial advisor. At the outset it seems difficult to find an objective answer to these questions. However, if one were to ask Google Baba one will find that some good research work has already gone into this subject. One such research is from Vanguard Inc. which is a leading Investment company managing over 3 Trillion USD of assets in USA. As per Vanguard, a financial advisor adds over 3% of portfolio returns to the investor on an annual basis. The Vanguard research paper can be downloaded at https://www.vanguard.com/pdf/ISGAA.pdf

This study was done predominantly for financial advisors of the USA. If one were to extrapolate this value for the financial advisors of India, the value might be much higher. Lets first try to understand the salient points of the work done by Vanguard Inc:

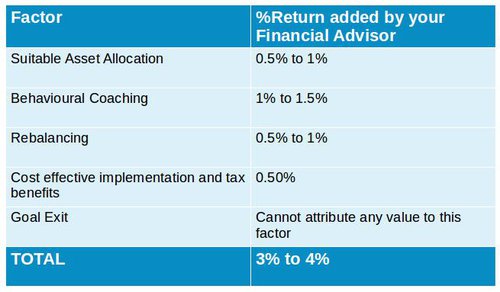

Suitable asset allocation: There are four main asset classes namely equity, debt, commodities and real estate. Most of the investors have a tilt towards one or two of these asset classes. For example, someone may be over-allocated towards real estate. This affinity could be due to various reasons. But the most prominent reason is behavioural tendencies and past experience. A skewed asset allocation not only reduces the return of the overall assets but also increases the risk substantially. Your financial advisor helps you to come up with an appropriate asset allocation strategy depending on your age, risk taking capacity, goal duration etc. The market risk can be reduced significantly and the returns can be enhanced by following a suitable asset allocation strategy. Vanguard attributes an additional value of 0.5% to 1% to this factor.

Behavioural coaching: As an investor we have a tendency to panic when the market falls. As our hard earned money is at stake, we tend to liquidate our stocks. Your financial advisor has expertise in this domain, so buying and selling is done on the basis of micro and macroeconomic factors affecting the investment. As per Vanguard, this is one of the most important value that your financial advisor brings to the table. Most of the investment decisions go wrong due to wrong emotional decision after a period of relative under-performance. Since your financial advisor’s money is not directly at stake, she can take an objective decision which is based on her expertise and not on emotions. Vanguard attributes an additional value of 1% to 1.5% to this factor.

Rebalancing: This involves periodically buying and selling of assets in the portfolio. This is to maintain the original desired level of asset allocation. This is a very powerful practice often underestimated by most of the investors. For investments that have given negative returns in the review period, the strategy enables the financial advisor to buy low. Likewise, this strategy helps one to book profits from a particular asset class after it has run up in a short duration of time. Hence, the age old principle of “BUY LOW and SELL HIGH” is in-built into this strategy. Vanguard attributes an additional value of 0.5% to 1% to this factor.

Cost effective implementation & Taxation benefits: Your financial advisor helps you to invest into products that are relatively low cost and have much better past track record. For example, any good financial advisor will never advise you to invest into insurance products. They would generally advocate that insurance and related products should be used for covering the risk of life or health, rather than for growing your money. Similarly, within the core investment products, they will choose products that are of lesser cost. For example, each mutual fund has a different expense ratio. Expense ratio is the cost of managing the mutual fund. Finding the right mutual fund with low expense ratio and a good management team is a tedious process. Your financial advisor has an expertise in this domain. Your financial advisor also helps you to minimize your tax outgo by creating a more tax efficient investment portfolio for you. She will try to find strategies that will be lower on tax and take advantages of existing tax laws to deliver higher post tax returns for your family. Vanguard attributes an additional value of 0.5% to this factor.

Goal Exit: This is another very important point that is missed by most of the investors. Often investors try to spend a lot of time and energy to enter a particular investment product. However, they tend to discount the need to exit such investments based on their goal completion. For example, if one needs money for a goal which is three years away, then irrespective of the market conditions, the money should be taken out from a risky product and invested into low risk products like debt or fixed deposits. Your financial advisor will help you plan and execute such a strategy. This will result into a lot of comfort for you and eventually brings peace of mind for you. Vanguard did not attribute any objective value to this factor.

To summarize, total value of the above factors as researched by Vanguard Inc. comes out to the following:

How similar or different are these factors to Indian investors?

Though the above study was done for US markets, we believe that they have a lot of similarity for Indian conditions as well. The gap between fixed instrument returns and financial market returns is much higher in India as compared to US. Hence, if we were to extrapolate the above findings to Indian conditions, the value that your advisor is adding is likely to be in the range to 5% as compared to 3% in the US.

You can also read about the advantages of financial advisor

How much fees is justified to be paid to the financial advisor?

Some popular fee models that are currently prevalent in India are as follows:

AUM based fee model: The financial advisor charges a percentage of fees for the assets that she manages for an investor. Typically the fees ranges between 1% of AUM to 1.5% of AUM

Fixed Fee model: Financial advisor charges a flat annual fee based on the amount of time that she is spending to manage an investor’s account / relationship

Profit sharing model: There are some fee models that are based on the outcome of profits earned on the investments. This fee model is, however, under dispute as SEBI in its recent guidelines has discouraged use of this fee model for SEBI Registered Investment Advisors. As per SEBI, this fee model is more suitable for portfolio managers who just manage funds irrespective of risk profile of the investor.

Our view is that there is no clear answer to this question. An investor needs to judge the value that her financial advisor is adding to her financial journey. Based on what is comfortable to you and your financial advisor, you can choose amongst one of the above fee models.

Get Expert Financial Advice

Book an introductory call with our Certified Financial Planner to explore how we can help you achieve your financial goals.

Book Your Appointment