What’s The Difference Between Financial Planning and Investment Management?

Financial planning is the process of mapping your entire financial life, your goals, income, expenses, insurance, taxes, and retirement into a structured roadmap. Investment management is the ongoing activity of selecting, monitoring, and rebalancing a portfolio to grow your money. Financial planning tells you where you need to go. Investment management moves you there. One without the other leaves your money either parked, directionless, or in motion toward the wrong destination.

What Is Financial Planning?

Financial planning is a structured process that evaluates your complete financial situation and builds a strategy to achieve your life goals.

It is not just about picking mutual funds or opening a PPF account. It covers every dimension of your financial life: how much money you need to retire, how to fund your child's education, whether your insurance cover is adequate, how to reduce your tax liability, and how to protect your wealth if something unexpected happens.

The financial planning process typically moves through six stages:

- Assess your current situation: income, expenses, existing assets, liabilities, and insurance cover.

- Identify your financial goals: retirement corpus, child education fund, home purchase, and any other milestones with a timeline and a number attached.

- Analyse the gap: how much you need versus how much you are on track to accumulate.

- Build the strategy: how much to save, in which instruments, over what period, with what asset allocation.

- Implement the plan: put the investments, insurance, and tax structures in place.

- Review and revise the plan annually or whenever your life changes.

These six steps form the backbone of any structured financial plan. If you want to understand the specific goals each step serves, read our detailed breakdown of the objectives of financial planning and how they translate into real financial decisions.

What Is Investment Management?

Investment management is the active practice of building and maintaining an investment portfolio in line with a defined objective.

It includes selecting which funds, stocks, bonds, or other instruments to invest in, deciding on asset allocation across equity, debt, and alternatives, monitoring performance against benchmarks, rebalancing when market movements shift the allocation, and making changes when a fund underperforms or a better option becomes available.

The investment management process generally follows this sequence:

- Define the investment objective: growth, income, capital preservation, or a combination.

- Establish risk tolerance: the level of volatility the investor can absorb without making poor decisions.

- Build the portfolio: select instruments across asset classes based on the objective and risk profile.

- Monitor performance: track returns against relevant benchmarks at regular intervals.

- Rebalance: restore the target allocation when market movements cause drift.

- Adjust: respond to changes in the investor's life circumstances, goals, or market conditions.

Investment management is a continuous activity. It does not end once the portfolio is built.

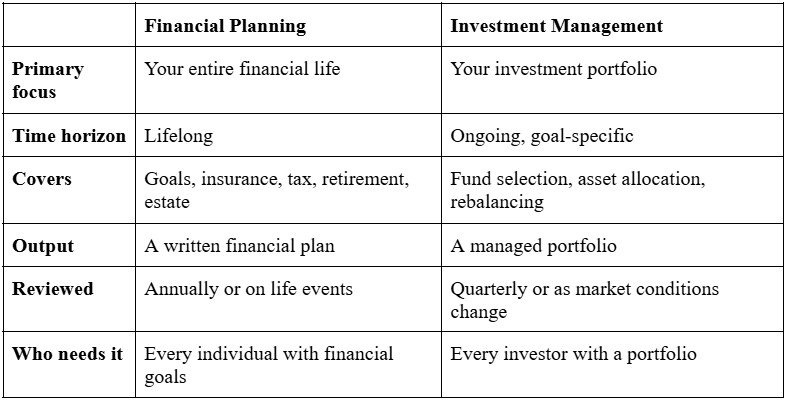

What Is the Difference Between Financial Planning and Investment Management?

The clearest way to state it: financial planning is strategic, investment management is tactical.

Financial planning defines the destination, how much money you need, by when, and for what purpose. Investment management is how you get there, which instruments carry your money, at what pace, and with how much risk.

Here is a direct comparison:

The two are not alternatives. Investment management is one component of financial planning, the execution layer that sits beneath the strategic plan.

What Is the Difference Between Financial Planning and Wealth Management?

Wealth management is a broader service that combines financial planning, investment management, tax strategy, estate planning, and sometimes legal advisory under one engagement.

The difference between financial planning and wealth management is primarily one of scope and client segment. Financial planning focuses on building and executing a roadmap for your financial goals. Wealth management adds layers, managing complex tax structures, multi-generational wealth transfer, business succession, and high-net-worth investment strategies.

For most salaried urban professionals in India, comprehensive financial planning that covers goals, insurance, taxes, and investments is sufficient. Wealth management is typically relevant when assets become large enough and complex enough to require specialist input across multiple financial domains simultaneously.

The difference between financial management and financial planning is different again. Financial management in the personal finance context refers to the day-to-day management of income, expenses, budgets, and cash flow. Financial planning takes that foundation and builds a long-term strategy on top of it.

Why Most Indian Investors Get This Wrong

Here is the pattern that financial advisers in India encounter repeatedly: an investor builds a portfolio of eight to twelve mutual funds, reviews performance every few months, switches out underperformers, and believes they are doing financial planning.

They are not. They are doing investment management, and often not well, because frequent switching based on short-term returns is one of the most reliable ways to erode long-term wealth.

According to the PGIM India Mutual Fund Retirement Readiness Survey 2025, retirement has surged to the top financial priority for Indian families, yet only 37% of respondents currently hold a retirement plan, down from 67% in 2023. The gap between aspiration and preparation is not caused by a lack of investment products. India has thousands of mutual funds, ETFs, PMS options, and digital investment platforms. The gap exists because most people are managing investments without a plan that tells them what those investments are supposed to achieve.

As of December 2024, the number of SEBI-registered investment advisers (RIAs) in India had fallen below 1,000, serving a country of 1.4 billion people. The shortage of qualified, fiduciary financial planners means that most investors either receive product-driven advice from distributors with commission incentives or attempt to manage everything themselves using DIY platforms that offer investment execution but no planning layer.

This is the core distinction that most content in this space fails to make clearly: investment management without a financial plan is navigation without a destination. You may be moving efficiently. You have no way of knowing whether you are moving in the right direction.

The Financial Planning Process vs The Investment Management Process: Side by Side

Financial planning asks:

- How much do I need to retire comfortably? If you are approaching or already in retirement, our dedicated guide on financial planning for senior citizens covers income allocation, the benefit of compounding in retirement, healthcare costs, and tax minimisation strategies for retirees.

- Is my family protected if I am no longer around?

- Am I paying more tax than I should?

- Am I on track for my child's education expenses? For parents navigating this question in practice, our guide on financial planning for new parents covers education cost projections, the impact of delays, and how to structure a goal-based portfolio from day one.

- What happens to my assets after I am gone?

Investment management asks:

- Is this fund outperforming its benchmark?

- Should I shift from large-cap to mid-cap given current valuations?

- Has market movement pushed my equity allocation above my target?

- Is this debt fund suitable for my three-year goal?

Both sets of questions matter. But the first set must be answered before the second set has any meaning.

How FinAtoZ Approaches Financial Planning and Investment Management

FinAtoZ is a SEBI-registered investment adviser (INA200006628) and AMFI-registered firm (ARN: 114771). It operates on a fee-only, fiduciary model; advisers do not earn commissions from any product they recommend, which removes the structural conflict of interest that affects most bank-based and distributor-led advisory.

The firm's engagement begins with financial planning, not fund selection. Every new client goes through a dedicated one-on-one session with a Certified Financial Planner to document current financial position, quantify each goal with a timeline and a target number, and produce a written financial plan before any investment recommendation is made.

Investment management follows the plan, not the other way around. Portfolio construction uses FinAtoZ's proprietary 4P1R Research Process, evaluating funds across Philosophy, Process, People, Performance, and Price, and Finametrica's validated risk-profiling tools to ensure the portfolio is calibrated to the client's actual risk capacity.

Portfolios are reviewed annually, and the financial plan is updated whenever a client's circumstances change: a salary increase, a new family member, a career shift, or a change in a goal timeline.

Shahul Hamhiran, a Financial Services professional, described the onboarding experience this way on FinAtoZ's testimonials page: the clarity and thoroughness in understanding not just what to do but how to get there gave him significant comfort, because other advisers had focused on products rather than on his financial goals.

That distinction, goals first, products second, is the operational difference between financial planning and investment management in practice.

If you want to understand what to look for before engaging any financial planner, including credentials, fee structures, and the right questions to ask, read our step-by-step guide on how to choose a financial planner in India before booking your first call.

If you want to understand how these two services would be structured for your specific situation, you can book an introductory call with a Certified Financial Planner on the FinAtoZ website.

Frequently Asked Questions

What is the difference between financial planning and wealth management?

Financial planning builds a structured roadmap to achieve your financial goals, covering investments, insurance, tax, and retirement. Wealth management is a broader, typically higher-cost service for clients with significant or complex assets, adding estate planning, multi-generational tax strategy, and business succession services to the financial planning foundation.

What is the difference between financial management and financial planning?

Financial management refers to the day-to-day management of income, expenses, and cash flow. Financial planning builds on that foundation and develops a long-term strategy to achieve specific financial goals throughout your lifetime.

Do I need both financial planning and investment management?

Yes. Financial planning without investment management gives you a plan with no execution. Investment management without financial planning gives you a portfolio with no direction. The two work together: the financial plan sets the goals, and investment management builds and maintains the portfolio that works toward them.

Is financial planning only for wealthy people?

No. Financial planning is relevant for any individual with income, goals, and financial decisions to make, which includes most working adults. SEBI-registered investment advisers in India charge fees starting from ₹12,000–₹15,000 annually for planning services, making structured financial advice accessible beyond the high-net-worth segment. FinAtoZ's onboarding fee starts at ₹24,000 for a comprehensive financial plan, including an existing asset review, insurance assessment, and a goal-based roadmap.

Get Expert Financial Advice

Book an introductory call with our Certified Financial Planner to explore how we can help you achieve your financial goals.

Book Your Appointment