Retirement Bucket Strategy – “No More Retirement Anxiety”

An efficient way to fund your post-retirement life:

Anshuman Meher | Wealth Manager | FinAtoZ – RightFocus Investments Pvt. Ltd.

Do you need a regular income post-retirement? Contrary to popular belief, we don't need regular income but rather a steady cash flow in our retirement years that can serve our day-to-day expenses.

The solution is to have a sound retirement financial plan and a diversified portfolio that protects one from inflation and the risk of outliving his/her retirement assets. The plan should be tailor-made to fit individual needs and reviewed regularly. The most effective and efficient way to build this corpus is to use the bucket strategy to plan the future cash flow from the retirement corpus.

What is a bucket strategy in retirement planning?

When one retires with a significant savings corpus, it is easy to become complacent and assume everything will be fine going forward. However, there are a couple of reasons why this frame of mind may not work:

a) You no longer have a monthly income except for your savings.

b) Emergencies can happen at any time, and inflation will erode the purchasing power of your money over time, especially in the long term.

c) Additionally, the safest investments typically have the lowest returns, while riskier investments offer the potential for higher returns.

So, how can we ensure that one:

a) Don't take unnecessary risks with their life savings.

b) Have enough money each month to live comfortably.

c) Can ensure the expenses of unexpected emergencies.

d) Have the required insurance coverage.

That is where the bucket strategy comes in. This strategy divides the retirement portfolio into different buckets, considering one's financial goals and investment horizon by ensuring liquidity and risk-adjusted return.

The buckets can be categorized as follows:

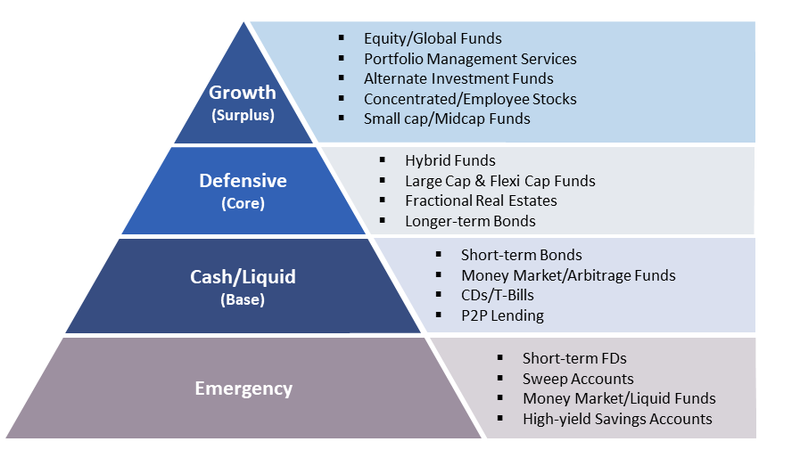

Bucket 1 – Emergency Bucket:

An emergency fund is the foundation of any sound financial plan. It provides a safety net to cover unexpected expenses and emergencies that may arise at any time.

Now the question arises: "How much and where should you save your emergency fund?"

For most people, an emergency fund of Rs 15-25 lakh is sufficient. Depending on individual circumstances, such as having older dependents or medical conditions not covered by health insurance, the amount needed may vary. A good rule of thumb is to save 6-12 months of living expenses in emergency corpus.

The best place to invest your emergency fund is in liquid assets that can be easily accessed when needed. Some good options include:

a) High-yield savings accounts

b) Money market/Liquid mutual funds

c) Short-term FDs

d) Sweep accounts (excess funds in SB account get switched automatically to an FD /liquid fund)

Additional tips:

a) Review the emergency fund regularly to ensure it meets your needs adequately.

b) If your financial situation changes, adjust the emergency fund accordingly.

c) Consider a recurring deposit (RD) to build an emergency corpus gradually.

Bucket 2 – Cash/Liquid Bucket:

The purpose of the cash bucket is to cater for the living expenses for the next three years, which are inflation-adjusted and based on the annual expenses in the first year of retirement while keeping similar living standards. Any retirement income, rent, interest payments, dividends, etc., should be adjusted to the annual expense value before finding out the amount to be saved in this bucket.

The funds in this bucket are mostly liquid and should cover the inflation growth with low-risk and stable returns as it will cover your immediate expenses. Some suggested investments would be - your savings bank account, FDs, money market/arbitrage funds, short-term bonds, P2P lending or any other liquid investments.

Bucket 3 – Defensive Bucket:

The defensive or medium-term bucket contains 4 to 7 years' worth of expenses. Money in this bucket should continue to grow to keep pace with inflation and help you achieve your short-term and medium-term goals, whether it's that long-awaited vacation or pursuing your passions. Keeping it too safe might make it easier to beat inflation, and being too risky might result in losses. Common medium-term investments include longer-maturity bonds and CDs, large-cap funds, hybrid funds, preferred stocks, REITs and more.

Income generated from this bucket can be used to refill the Cash bucket as its assets are drawn down.

Bucket 4 – Growth Bucket:

Now that we have already planned for the emergency fund and cash flow requirement for the first seven years post-retirement, the final segment of your retirement plan should primarily focus on investments geared towards growth.

The growth bucket represents the aspirational portion of the pyramid. This bucket is for long-term investments that help generate alpha+ returns. The returns generated from this bucket serve to replenish both cash and defensive buckets.

Growth bucket investments are invested in riskier assets that may be volatile in the short term but have growth potential over ten years or more. With the retirement bucket strategy, your long-term bucket should have a diversified portfolio of stocks and related assets. It should be allocated across domestic and international investments ranging from micro and small-cap to large-cap stocks.

Given the anticipation of superior long-term performance of this bucket, it becomes essential to rebalance the overall portfolio periodically to prevent an undue concentration in equities.

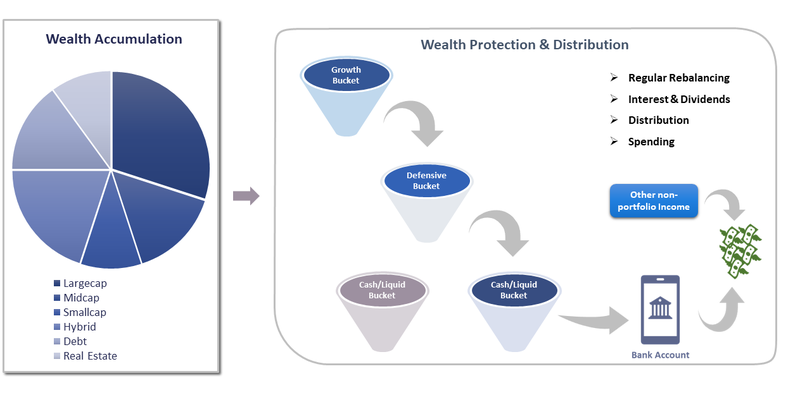

Maintenance & Rebalancing of Retirement Buckets:

Managing the retirement bucket strategy involves some intricacies, especially with the periodic rebalancing. One should treat the rebalancing of the three retirement buckets as similar to any other portfolio. If the long-term bucket multiplies rapidly, shift funds to the cash and defensive buckets to maintain the target allocations. Determine the minimum balance for the cash bucket before selling off holdings in the other two buckets to replenish it.

In times of a significant stock market decline, one can refill the cash bucket from the defensive portfolio instead. That's why a minimum of 4-7 years cushion is required in the medium-term bucket. As stocks rebound, sell assets from that bucket to restore funds. This strategy allows selling long-term assets at high prices and buying at low prices.

Like any other investment strategy, the retirement bucket strategy has its pros and cons. Here are some of the benefits and drawbacks of the retirement bucket strategy:

Benefits of the Retirement Bucket Strategy:

- The Retirement Bucket Strategy offers a sense of security for retirees worried about future investment performance.

- It minimizes the need to sell during market downturns. Instead, if stock values decline, retirees can tap into other funds like cash reserves while keeping stock market investments positioned for long-term growth opportunities.

- This approach provides peace of mind for some investors, allowing them to stay invested even in volatile markets.

Drawbacks of the Retirement Bucket Strategy:

- Regular monitoring is crucial for the retirement bucket strategy, and adjustments may be necessary based on market conditions. If neglected, the buckets may not achieve the expected results.

- Setting up and managing the retirement bucket strategy independently requires significant effort, and there's a risk of missing potential opportunities.

In conclusion, the Retirement Bucket Strategy provides a sense of security for retirees. Still, the intricacies involved in monitoring, adjusting to market conditions, and optimizing the strategy highlight the crucial role of expert guidance. Consulting with a financial professional can be instrumental in effectively implementing and managing the retirement buckets, ultimately paving the way for a more secure and well-rounded financial freedom.

Establishing a robust retirement financial plan involves several key elements:

- Early Savings: Initiate retirement savings early to leverage the compounding effect and allow your money ample time to grow.

- Asset Allocation: Diversify your portfolio across various asset classes, including stocks, bonds, and cash, to mitigate risk and optimize returns.

- Emergency Fund: Maintain a sizable cash reserve equivalent to at least three to six months of living expenses to cover unforeseen financial challenges.

- Insurance Coverage: Ensure adequate insurance coverage for protection against potential financial setbacks resulting from illness, injury, or death.

- Income Generation: Ensure your investments generate sufficient income to cover monthly expenses, with a focus on income-producing assets like dividend-paying stocks and bonds.

- Regular Portfolio Rebalancing: Adjust your portfolio over time to align with changing risk tolerance and evolving financial needs as you age.

- Spending Monitoring: Keep a close eye on spending habits, making necessary adjustments to maintain financial stability and avoid exceeding your means.

By incorporating these practices, one can develop a well-rounded retirement financial plan, paving the way for achieving retirement goals and enjoying a financially secure and comfortable retirement.

Get Expert Financial Advice

Book an introductory call with our Certified Financial Planner to explore how we can help you achieve your financial goals.

Book Your Appointment