How Much Should You Save Every Month?

Most salaried professionals in India have a rough idea of their salary. Save something. Maybe 10%. More if there is money left over at the end of the month. That approach produces inconsistent results and, more often than not, a savings rate that quietly erodes over time as expenses rise.

This blog answers a specific question: how much of your salary should you save each month, and why the answer isn't the same for everyone.

The Number Most People Start With: The 50-30-20 Rule

The 50-30-20 rule is the most widely cited savings framework. It allocates 50% of take-home pay to needs, 30% to wants, and 20% to savings and investments.

It is a reasonable starting point. But it was designed for a general audience, not for a salaried professional in an Indian metro who has a specific retirement date in mind, a child's education to fund, and a home loan running in the background.

For many urban professionals with higher incomes, 20% is too low. For someone early in their career with a modest salary and high fixed costs, 20% may temporarily be out of reach. The rule gives you a direction. It does not give you a number.

Why a Flat Percentage Misses the Point

What percentage of salary should be saved is the right question. But the answer depends on four variables that are specific to you:

Your Age and Time Horizon

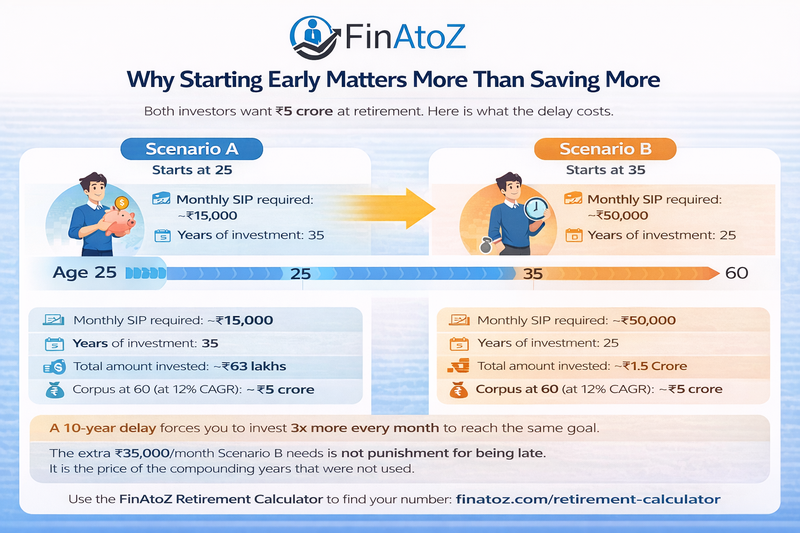

Someone who starts saving at 25 needs to save a smaller percentage of their salary to reach the same retirement corpus as someone who starts at 35. Time is the most powerful variable in the equation. A ten-year delay can require you to more than double your monthly savings to achieve the same outcome.

Your Goals and Their Timelines

A child's education over 12 years, a home purchase over 5 years, and retirement over 25 years all have different cost trajectories and required monthly contributions. Adding them up gives you your actual savings target. That number may be 25% of your salary. It may be 40%.

Your Current Liabilities

If you are servicing a home loan, your EMI is effectively a form of forced saving, since you are building an asset. But it also reduces your investable surplus. The percentage of salary that should go toward investments will differ for someone with an EMI of ₹40,000 versus someone with none.

Inflation and Return Assumptions

Saving ₹10,000 a month in a savings account is not the same as investing ₹10,000 a month in an equity mutual fund. The corpus you built over 20 years differs several times. The savings rate question is inseparable from the investment question.

What the Data Says About Where India Actually Stands

As told by Business Standard, according to the Reserve Bank of India's Annual Report 2024–25, India's household financial savings rebounded to 5.1% of gross national disposable income in 2023–24, after falling to a multi-year low the previous year.

That rebound sounds encouraging. It is not. The figure reflects the average Indian household's savings in financial instruments after accounting for liabilities. For a salaried professional aiming for financial independence, saving 5% of income in financial assets is nowhere near enough.

The pension picture is starker. According to the Mercer–CFA Institute Global Pension Index 2025, EPFO, NPS, and government-backed schemes together cover less than 25% of India's workforce, one of the lowest inclusion rates globally. India ranks 45th out of 47 countries in the index, with an overall score of 43.8, retaining a 'D' grade.

India's Economic Survey 2024–25 noted that just 5.3% of the total population is covered by NPS and APY combined.

What this means in practice: the vast majority of salaried professionals in India are relying entirely on their own retirement savings, without a reliable pension safety net. The savings rate question is therefore not academic. It is the only plan most people have.

A More Useful Framework: Save by Goal, Not by Rule

Rather than applying a flat percentage, calculate your required savings from the goals backward.

- Start by listing every major financial goal: retirement corpus, child's education, home purchase, and a contingency fund.

- Assign a cost and a timeline to each.

- Then use a compounding calculator to determine the monthly SIP or savings required for each goal at a conservative expected return.

- Add those monthly amounts up. Divide the total by your take-home salary. That is your personal savings rate.

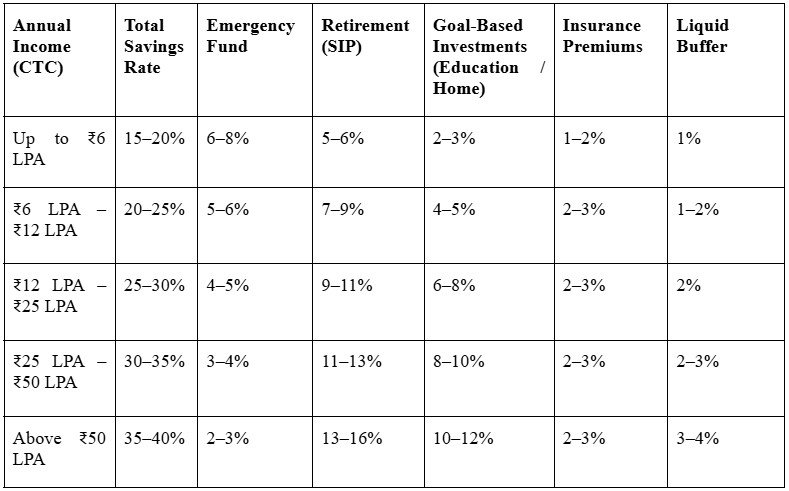

For most salaried professionals in Indian metros, this exercise accounts for 25% to 40% of take-home pay. That is meaningfully higher than the 20% the 50-30-20 rule suggests. And it is specific to you, not to a generic template.

Use the FinAtoZ Retirement Calculator to run this calculation for the retirement component of your goals. It adjusts for inflation and gives you a monthly savings target based on your current age and desired retirement age.

Savings Rate vs. Investment Rate

Saving is setting money aside. Investing is putting that money to work against a specific goal at a specific return. A savings account earns 3–4%. Over the long term, an equity mutual fund has delivered significantly more. These are not equivalent.

The question is not only how much of your salary you should save, but also how you should save it. It is: how much of your salary should be actively invested against a plan, and how much should sit idle as a buffer?

FinAtoZ's position, built on working with salaried professionals across India, is this: your emergency fund should cover six months of expenses and be kept liquid. Everything above that should be deployed against a goal. Idle savings above your emergency buffer are not safe. They are quietly losing value to inflation.

This means your monthly savings rate has two components. The first is the temporary emergency fund build-up phase. The second is the ongoing investment rate, which should be goal-sized and permanent.

How to Save Money from Salary Every Month: The Practical Structure

Knowing your target savings rate and actually maintaining it are different problems. Here is a structure that works:

Automate before you spend. Set up SIP mandates that debit on the 1st or 2nd of each month, the day after your salary credit. Do not wait to see what is left over. What is automated gets invested. What is left in the account gets spent.

Increase your rate when your salary increases. Most professionals keep their savings fixed as their salaries grow, so their savings rate falls each year. Commit to directing at least 50% of every salary increment toward investments. This is called the savings rate escalation approach, and over a 15-year career, it produces compounding outcomes that a flat SIP cannot replicate.

Separate your accounts. Maintain one account for monthly expenses, one for your emergency fund, and one from which your SIPs draw. Mixing them creates the illusion that money is available when it is not.

What FinAtoZ Clients Do Differently

FinAtoZ is a SEBI-registered investment adviser (INA200006628) operating on a fee-only, fiduciary model. Unlike commission-based distributors, FinAtoZ earns no commission on the products it recommends. Every recommendation is aligned exclusively with the client's goals.

For clients whose savings rate has historically been informal or inconsistent, the planning process begins with a one-on-one meeting with a dedicated CFP-certified adviser. The output is not a generic financial plan. It is a specific monthly savings target, broken down by goal, with a clear investment plan behind each number.

FinAtoZ's advisory is available for an annual fee of 1.2% of AUM, plus a one-time onboarding charge. Details are available on the FinAtoZ pricing page.

For a broader view of how goal-based planning works in practice, read Factors Affecting Investment Decisions and Net Worth vs. Income: What Matters More and Why.

Frequently Asked Questions

How much of my salary should I save when I start?

Start with at least 20% of your take-home salary. If your fixed costs are high, start with whatever you can sustain without breaking it after two months. A consistent 15% beats an inconsistent 30%. Increase the rate by 2–3 percentage points each year until you reach your goal-based target.

What percentage of salary should be saved for retirement specifically?

Run the retirement calculation backward from your desired retirement corpus. As a rough benchmark, a 30-year-old aiming to retire at 60 with a corpus of ₹5 crore in today's terms needs to invest approximately ₹15,000–20,000 per month, assuming a 12% annual return on equity. The exact number changes with your lifestyle costs and inflation assumptions.

Should I save more or invest more?

Once your emergency fund is in place, direct all surplus toward investment. Saving without investing is a plan that loses to inflation every year.

How much salary should I save if I have a home loan running?

Your EMI is a financial obligation, not an investment. Treat it separately from your savings rate. Continue to direct at least 20–25% of take-home pay toward goal-based investments even while servicing a loan.

Does the 50-30-20 rule work for Indian salaries?

It works as a starting framework but consistently underestimates what is required for retirement in India, where no meaningful pension safety net exists for most salaried workers. Treat 20% as a floor, not a target.

Get Expert Financial Advice

Book an introductory call with our Certified Financial Planner to explore how we can help you achieve your financial goals.

Book Your Appointment